By Vita on November 6, 2023

Several years ago, the Department of Labor (DOL) investigated Prudential Life Insurance Company's practices involving voluntary, supplemental group life insurance coverage. The issue was that premiums were paid by plan participants (via salary reduction) for extended periods of time, but after participants died, claims were denied on the grounds that the participants failed to provide evidence of insurability at the time they applied for the insurance.

Parallel investigations found that other life insurers also engaged in similar practices. The marketplace reality is that, absent this recent spotlight on these issues, many insurance companies have been guilty of varying degrees of sloppiness in syncing payroll deductions with underwriting approvals.

Settlement

In the settlement agreement, Prudential agreed to revise this practice and ensure that beneficiaries are not harmed in the event employers fail to verify that participants' evidence of insurability was approved prior to collecting premiums. The specifics of the settlement prohibit Prudential from denying a beneficiary's claim based on the lack of evidence of insurability when premiums were collected for more than three (3) months. In addition, formerly denied claims based on lack of evidence of insurability have been reprocessed.

Forward Guidance to All Insurance Companies

The DOL encouraged all insurers to examine their practices to ensure they are not engaged in similar conduct. Practically, it's more correct to say the DOL issued a stern warning as they are greatly concerned about protecting participants and curtailing these types of practices.

Roadmap for Employers

This activity signals the DOL's clear interest in protecting beneficiaries and presents an outline of DOL expectations for insurers and plan sponsors/employers in their administration of voluntary life insurance benefits.

Importantly, what is at issue here is not that insurance companies have the right to deny applications for supplemental, voluntary life insurance (if a participant does not pass the insurability requirements). Rather, it is a problem when employees perceive that they have insurance (because they are paying premiums via salary deductions), but their coverage is not really in force because their evidence of insurance documentation was not submitted.

The Often-Missed Step: Split Salary Deductions Into Two Parts

Historically, errors were made by simply starting premium salary deductions for the entire life insurance benefit and the employer forwarding the full premium to the insurance company rather than withholding and forwarding just the premium amount due for the Guaranteed Issue (GI) benefit level. This simple administrative error created a disparity in how much insurance an employee was paying for - and believed they owned - vs. how much had been approved by the insurance company.

The lesson for employers administering voluntary life insurance plans is that salary deductions must be split into two parts:

- The premium/salary deduction associated with any Guaranteed Issue (GI) insurance coverage, and

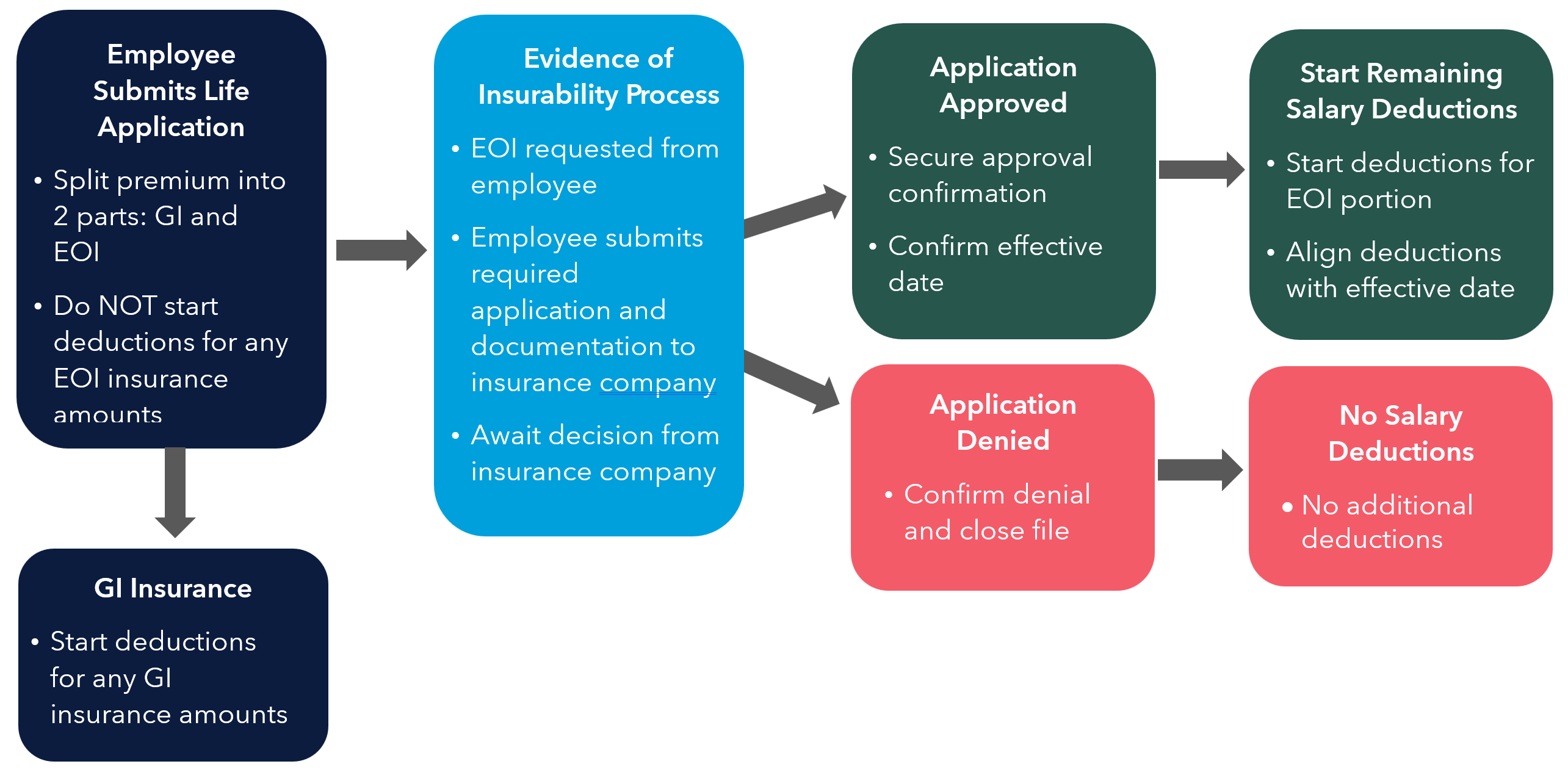

- The premium/salary deduction associated with any coverage that requires Evidence of Insurability (EOI). The following graphic illustrates the steps in the process for administration of this portion of the insurance coverage.

Employer Action Item

Employers should review their internal procedures as well as how they coordinate with their voluntary life insurance company. Specifically, employers should confirm that the following process elements are defined and implemented:

- Split Premium: Split voluntary life premium into two parts. Commence salary deductions for the guaranteed issue portion only and delay salary deductions for any portion of the premium attributed to insurance that requires evidence of insurability.

- Coordinate with Payroll: Coordination and communication between benefits and payroll departments are critical in defining and implementing processes.

- Confirm Insurance Decision: Obtain documentation of insurance approval (or denial).

- Commence Additional Deductions: Upon insurance approval, commence additional salary deductions.

References

The settlement agreement can be referenced here.

Healthcare and Employee Benefits in the Biden Era [Video]

401(k) Update: Q1 2024

.png)